The IEA’s Misplaced Techno-optimism

The third and final installment in a series of blogs on the IEA’s Special Report on gas and energy transitions. This blog discusses the IEA’s analysis of methane leakage and its faith in carbon capture and storage.

This is the third part of a 3-part blog series on the IEA’s Special Report, The Role of Gas in Today’s Energy Transitions. In Part 1, we discussed how the report shows that new gas-fired power capacity is losing ground to cheaper, cleaner renewables, and that coal-to-gas switching has played only a minor role in recent power sector emissions reductions. In Part 2 we exposed the problem with the report’s main policy prescription, more coal-to-gas switching.

This is the third part of a 3-part blog series on the IEA’s Special Report, The Role of Gas in Today’s Energy Transitions. In Part 1, we discussed how the report shows that new gas-fired power capacity is losing ground to cheaper, cleaner renewables, and that coal-to-gas switching has played only a minor role in recent power sector emissions reductions. In Part 2 we exposed the problem with the report’s main policy prescription, more coal-to-gas switching.

In this final installment, we will briefly explore the issues with IEA’s faith in technological solutions that would allow for gas production and consumption to keep growing, despite the diminishing space available for greenhouse gas (GHG) emissions.

Primarily, this post is about the IEA’s estimates of methane leakage, and its faith in carbon capture and storage (CCS). We will also touch very briefly on the report’s advocacy on coal-to-gas switching in energy sectors other than power generation, and the idea that building out gas infrastructure today may help a transition to so-called renewable gases in the future.

There’s a lot here and we won’t do all of these issues justice in this blog, but we intend to give a broad overview that should be helpful to understand what is going on here. Hopefully, we can shed some light on these complex issues.

Methane

First let’s deal with the IEA’s estimates of methane leakage. The IEA released a new Methane Tracker database as part of the Special Report. Its analysis of methane leakage from the global oil and gas industry underpins its assertion that gas can reduce emissions if it displaces coal in the energy system.

The IEA boldly states in the report that, “(g)as is nearly always better than coal on a lifecycle basis.” It claims that switching from coal to gas for power generation reduces emissions 50% on a lifecycle basis. The figure for switching for heat processes is 33%. Given that this is on a lifecycle basis and not just based on chimney stack emissions, these figures depend heavily on the calculations of methane leakage and how the impact of methane on climate is calculated.

Most readers of this blog are likely already aware that methane is the main component of fossil gas, comprising around 95% of the gas that is delivered to customers. What comes out of the ground is a mixture of gases including “wet” gases such as ethane, butane, and propane, as well as carbon dioxide (CO2), but most of these are removed before what we generally know as gas is transported through pipelines.

Methane is a super-potent GHG. It persists in the atmosphere for around 12 years before oxidizing into CO2, which persists for centuries. In order to compare its global warming impact (also known as radiative forcing) with CO2, which is the most abundant GHG, scientists use a Global Warming Potential (GWP) factor.

Lowballing Methane’s Global Warming Potential

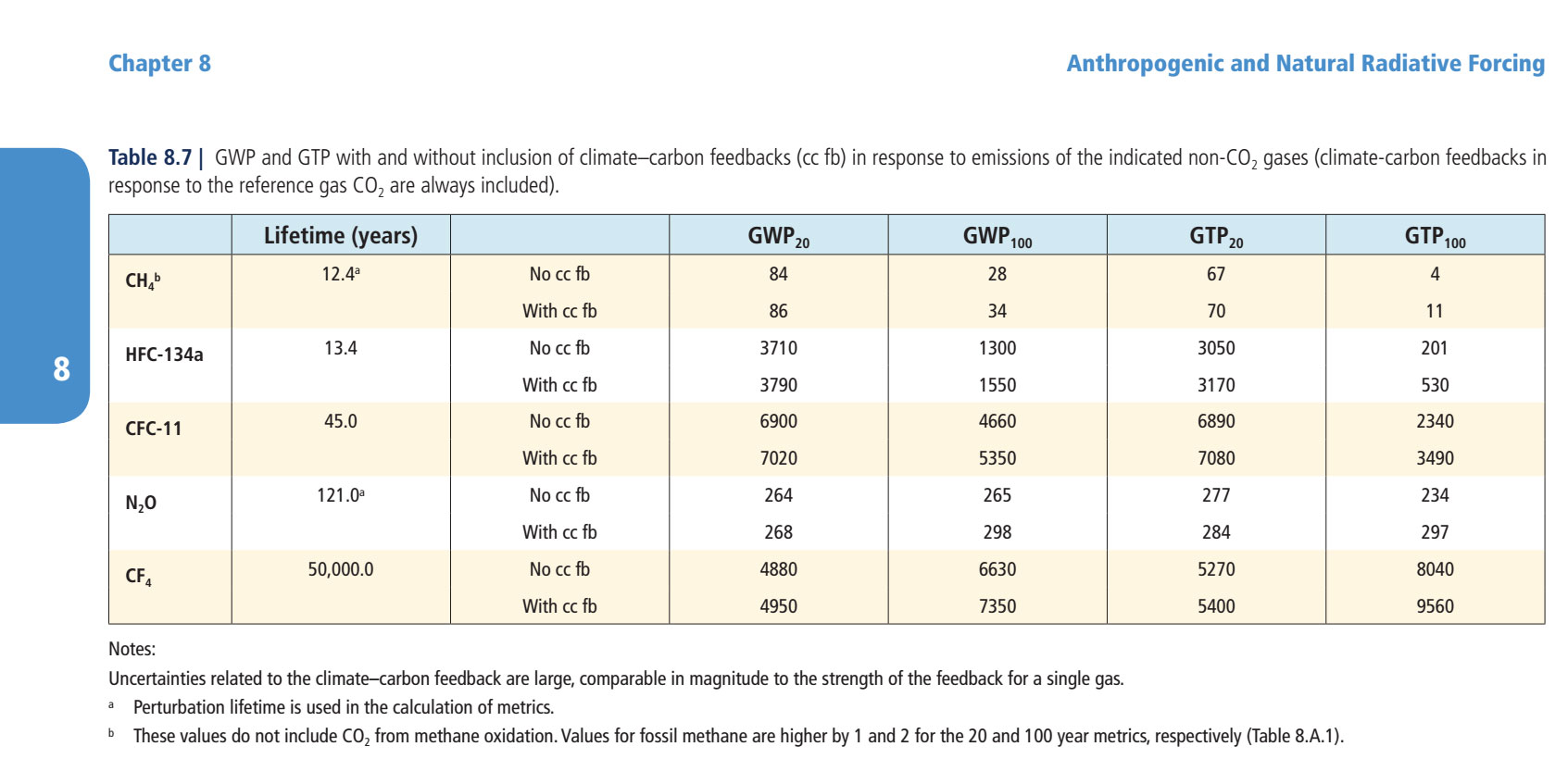

The Intergovernmental Panel on Climate Change (IPCC) uses two time periods for calculating GWP, but is generally agnostic about which one should be used. Over a 20-year period, the GWP for methane is 87, meaning the impact of a volume of methane over 20 years is 87 greater than the same volume of CO2. Over a 100-year period the GWP is 36. (Note that we include the factors for climate change feedbacks and oxidation. See this table from the IPCC AR5 report for details, methane is CH4 in the table).

{kind=link}

Industry and government generally use the 100-year GWP. This obviously substantially lowers their estimates of lifecycle emissions for gas compared with using the 20-year GWP. Climate advocates generally use the 20-year GWP. This makes sense because it is clear that rising methane emissions play a role in accelerating the climate impacts we’re currently seeing, not just the average impact over the next century.

In this report, the IEA uses a GWP of 30. There is no explanation for this. No reference for why the IEA uses that number is evident in the report. It may be that this is meant as a midpoint between the IPCC number that does not include climate-carbon feedbacks and oxidation (28), and the higher numbers of 34 or 36, depending on what you include (see the table here). The point here is that the IEA fails to reveal its reasoning. Neither does it note that there is uncertainty around this figure.

While there is not enough data in the report to judge how this affects the final lifecycle percentage difference figures, the claimed 50% and 33% emissions gap between coal and gas, here is a quick look at how the GWP can affect results.

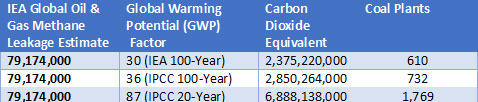

The difference between using a GWP of 30 or 36 in the calculations is relatively small compared to between a 20 and 100-year GWP, but still significant. When you put the numbers in the context of the average CO2 emissions from U.S. coal plants, using a GWP of 30 is like removing 122 coal plants from the estimated impact of methane emissions on climate. Conversely, using the IPCC’s 20-year GWP of 87 adds 1,159 coal plants.

Sources: IEA, IPCC, EPA

As the comparison of lifecycle emissions expressed in CO2 equivalents using a GWP factor is the main method for judging how much (if any) emissions reduction is achieved with coal-to-gas switching, the GWP factor used is clearly a fundamental parameter to get right. At the very least, some information on the ambiguity and ongoing study of methane’s GWP would make for a more honest assessment.

Indeed, research on methane’s radiative forcing has recently indicated that it is likely underestimated by the IPCC. A recent peer-reviewed paper indicated that the radiative forcing of methane may be at least 14% higher over the 100-year period than the IPCC numbers.

Leaky Leakage

The low GWP used by the IEA is just one way the IEA underestimates the climate impact of methane leakage. The other key variable is the methane leakage rate. This is the ratio of methane leaked to methane produced. Or essentially, how much methane is leaking. This is admittedly a very difficult thing to measure. Not least because the industry does a poor job of reporting it. But also because methane is an invisible gas, and the number of individual potential leakage points are, on a global scale, likely in the tens of millions. So effective regulatory monitoring is all but impossible.

The methodology behind the IEA’s methane leakage numbers is based on flawed U.S. government data. The IEA then extrapolates this flawed data globally. As documented in the World Energy Model Documentation, which outlines the methodology the IEA uses for its annual World Energy Outlook, the starting point for the entire IEA Methane Tracker is the U.S. Greenhouse Gas Inventory. This is the inventory of GHGs that the U.S. Environmental Protection Agency (EPA) records and submits to the IPCC annually.

When it comes to methane from the oil and gas industry, which could be leaking from any number of the hundreds of thousands (and growing) potential sources in the U.S., the EPA numbers have been repeatedly found to be underestimating the amount of leakage. The EPA has itself launched an evaluation of its methodology, after some of its data was found to be sourced from faulty equipment.

Numerous studies have used air monitoring and other means of measuring methane in the air around oil and gas production and many have estimated leakage rates to be significantly higher than the EPA estimates.

The IEA uses the EPA estimates as a starting point and then extrapolates leakage rates in other oil and gas producing countries based on assumptions around governance, regulatory regimes, the age of infrastructure, and the type of companies operating it.

There is no doubt that measuring methane leakage globally is a monumental task, so this is certainly one way to do it. But can this really be relied upon to provide such definitive statements as the IEA makes in this report? As mentioned above, rather than providing a range of possible methane leakage rates and corresponding lifecycle emissions estimates for gas compared to coal, the IEA confidently declares that gas is 50% cleaner than coal for electricity generation and 33% cleaner for heat processes. Despite the huge uncertainties in its methodology, no range is given.

The IEA does acknowledge the difficulty in measuring methane leakage and the potential for improvement. At the bottom of the methane tracker web page is a paragraph entitled “Improving the Data,” in which the IEA states that, “Emissions levels and abatement potentials are based on sparse and sometimes conflicting data, and there is a wide divergence in estimated emissions at the global, regional and country levels.” It then goes to mention that it is still in the process of compiling peer-reviewed papers on the issue and incorporating those into its methodology. An email is provided for readers to submit or recommend relevant literature. This seems odd as a database of peer-reviewed scientific papers on the issue has been in existence for years now and available here. This would be a good place for the IEA to start.

In summary, the IEA has chosen to ignore a vast body of peer-reviewed science on methane leakage in favor of developing its own methodology rooted in flawed U.S. government data. It may be a coincidence that this enables it to publish numbers on lifecycle emissions for gas and coal that mirror the established industry talking point that gas reduces emissions by 50% compared to coal when used for power generation. Whereas this figure was previously vulnerable to the fact that it was measured only at the power plant chimney stack, and did not include methane leakage along the gas supply chain, the new IEA numbers appear to address that critique while arriving at the same conclusion.

But They’ll Clean It Up

The other piece of the IEA’s strategy around methane is a pitch to the industry that a lot of leakage can be prevented at little or no cost. This is a noble cause. Methane leakage should be minimized, although it is doubtful that it can ever be entirely eliminated. But the problem with IEA’s pitch is that it seems divorced from the reality of the oil and gas industry to which it appeals. Particularly in the U.S., although certainly not exclusively, the industry does not operate in a way that inspires any confidence that it will clean up its act.

Methane regulations proposed by the Obama administration have been rolled back at the behest of industry players that have the ear of a compliant president. This includes companies like BP, that say one thing publicly and do the opposite when lobbying in the corridors of power.

The fact is that the industry has little incentive to value the methane it’s wasting when it’s so focused on production growth. Take, for example, the current situation in America’s most prolific oil and gas basin today: the Permian. The Permian is primarily an oil play, but a lot of gas is produced in the process of getting to the oil. This has caused such a glut of gas in Texas, and nationally given prolific gas production in Appalachia and elsewhere, that the price of gas has been negative in the Permian Basin for prolonged periods this year. Even as new pipeline capacity comes on line, gas prices are at historical lows and there is not much sign of change.

So gas is flared at record levels and, in the process, a lot of methane escapes unburned. In North Dakota, the situation is similar, in that the value of gas is such that it is cheaper to flare and vent it than to pipe it out. So the IEA’s case is undermined by the fact that in the Wild West culture of the U.S. oil and gas boom, the value of gas is too low for the economic incentives to address it to work.

Frankly, the IEA’s plans on methane seem like a sensible technocratic solution that everyone should get on board with but few ever will. At least not without strict regulatory enforcement, which is exactly what industry has resisted. It’s a little like gathering all the toddlers at a birthday party around a giant bowl of ice cream, giving them each a spoon and telling them not to spill any on their clothes, while you pop out for the cake. Maybe one or two sensible ones will try and comply, but there’s no way there won’t be a giant mess.

The truth is that the best way to prevent methane leakage in the oil and gas industry is to deny the permits for drilling in the first place. That is the only way to guarantee the methane stays where it belongs.

Carbon Capture & Storage

The other big piece of the IEA’s confidence in the longevity of gas in a carbon constrained world, is its faith in carbon capture and storage (CCS). The IEA believes that while it’s clear that emissions will have to be reduced beyond that which can be achieved through coal-to-gas switching, we can still rely on gas consumption growing because eventually CCS will deal with the emissions.

CCS is a technology that may work in theory to remove the majority of CO2 from the waste stream of a power plant, but it is far from clear that it will ever make economic sense to do it on a large scale. One recent study suggests that a carbon price of around $140 per ton would be needed to make retrofitting gas-fired power plants with CCS economic. The carbon price in Europe today is under 30 euro (about $33), and that is close to its high point for the past ten years.

CCS is energy intensive, requiring additional gas to run the capture facility, and it generally only removes around 80% to 90% of the CO2 in the waste stream. Factoring in the additional energy for the capture facility therefore means even lower efficacy. That, of course, also does not factor in the emissions, including methane leakage, of producing, processing, and delivering gas to the plant. CCS certainly isn’t a zero emissions solution.

Despite decades of government support for research, development, and pilot projects, only a handful of projects exist that capture CO2 from gas combustion rather than coal. Like the coal projects, none of them are really commercial without large public subsidies.

Even if we accept that some gas with CCS may be necessary to address hard-to-decarbonize industrial processes such as steel and cement, or that gas power plants will need to be kept around as back-up power generation, there is no justification for growing gas production in the hope that CCS will one day address emissions.

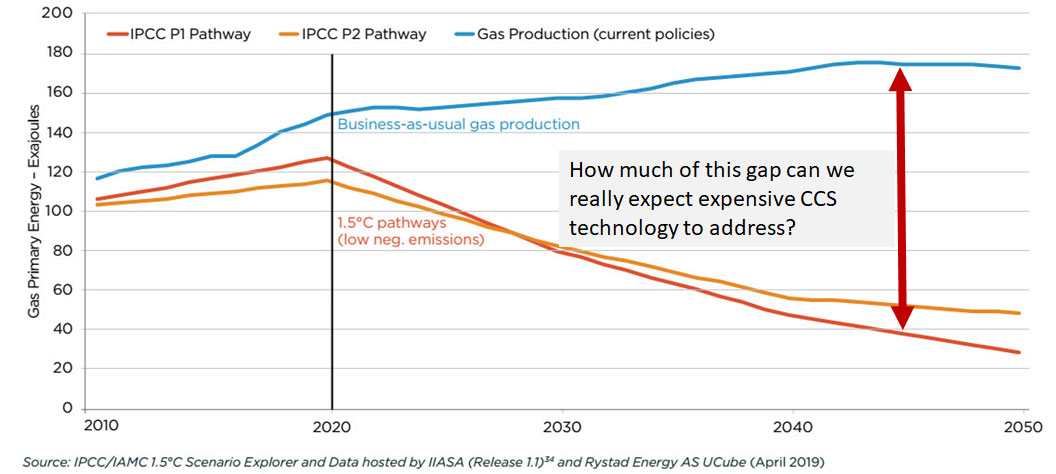

Looking at the chart below, which we have seen in part 2 of this blog series, and in our Burning the Gas ‘Bridge Fuel’ Myth report, it is clear that with CCS still a long way from commercial viability, it is wishful thinking that it will somehow bridge the gap between where gas production is heading and where emissions from gas need to be. CCS can in no way justify continuing along the business-as-usual path that the industry is pursuing, and which the IEA seems intent on supporting.

The Only Way is Down

The chart above makes it clear. Even assuming the industry gets methane leakage under control, which is unlikely, the only way for us to meet critical climate goals is to reduce gas use. CCS cannot change this fundamental trajectory.

Whether we’re looking at the power sector, or other sectors of the energy system including heat and industrial processes, we need to reduce our use of fossil fuels. There is no half measure that can make that easier.

The IEA report itself points out that locking in gas over the long-term is going to fail climate goals. So there needs to be more emphasis on other ways to reduce coal use in all energy sectors. The IPCC’s report on pathways to 1.5°C states that, “[s]ince the electricity sector is completely decarbonized by mid-century in 1.5°C pathways, electrification is the primary means to decarbonize energy end-use sectors.” In other words, a genuine decarbonization strategy will entail eliminating fossil fuels from the power sector while electrifying other energy sectors so that eventually the maximum possible proportion of energy is supplied by a combination of clean energy resources generating electricity.

There is no doubt that this is a tall order, and that there are difficult to decarbonize processes that cannot be easily converted to electricity. But investments must start today in genuine decarbonization. The first place to start is not fuel switching, but efficiency. Reducing the energy intensity of industrial processes can save money and energy with fast paybacks.

When it comes to difficult to decarbonize industrial processes, innovations in efficiency and fuel switching have to be made. The IEA report hints at the use of hydrogen for example and suggests that building out gas infrastructure today could smooth the path to future use of this gas. Manufacturing hydrogen from renewable energy is technically doable although currently very expensive. Costs may well come down with the scale of deployment, and that scale is potentially huge.

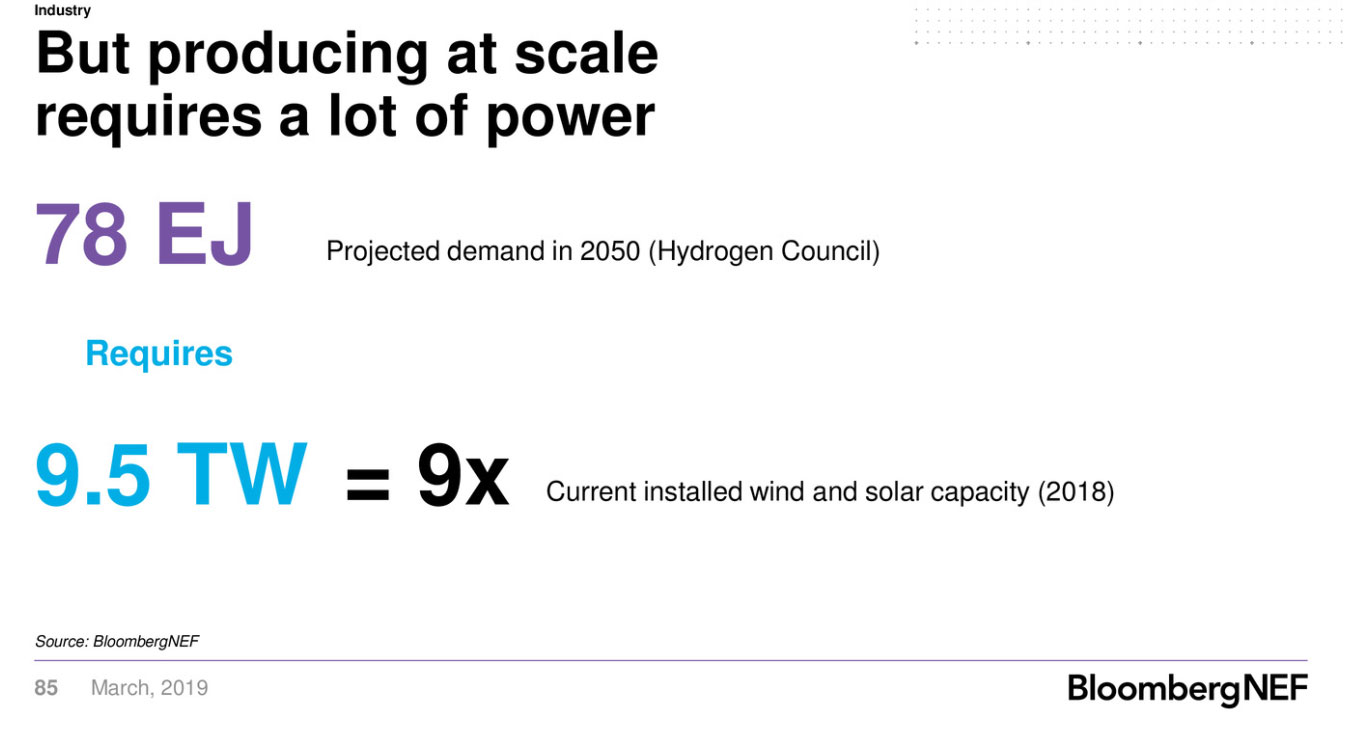

Bloomberg New Energy Finance (BNEF) recently calculated that meeting projected demand for hydrogen in 2050 with renewables will require roughly nine times the amount of wind and solar capacity installed globally in 2018 (see slide below). It is not impossible. But it does mean that the pace of renewable energy investment must greatly accelerate.

Therefore, rather than citing hydrogen as a Trojan horse for building out fossil gas infrastructure, the IEA should recognize that it is renewable energy infrastructure that should be urgently built out for a transition to hydrogen to take place.

In other words, true decarbonization will require a massive increase in renewable energy, far greater than we have seen yet, despite impressive recent progress. Achieving that is not facilitated by locking in gas production and its associated infrastructure.

If the IEA intends to facilitate the transition to a zero carbon energy system, it should cease advocating a further entrenching of the incumbent fossil fuel system, and advocate for maximum investment in efficiency and the clean energy infrastructure that it will clearly require.

This blog is part 3 of a three part series.

For more information and analysis on climate and gas, visit priceofoil.org/gas.